by Brianna Crandall — February 22, 2016—Data management challenges continued to escalate across all industries in 2015, according to global professional real estate services and investment management firm JLL’s (Jones Lang LaSalle) latest report on the top North American data center markets.

Multi-tenant data center providers experienced 6.1 percent growth and revenues of $115.3 billion. The industry is finding growth amid increased rate of “cloud” adoption and massive provider consolidation, coupled with the exodus of major telecommunications companies from the data center services sector.

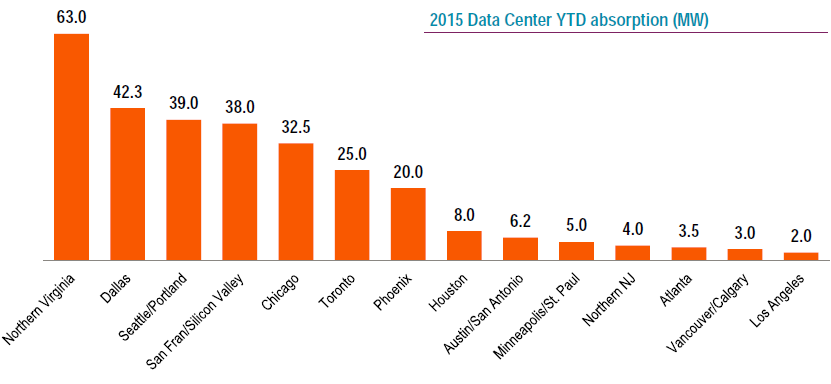

JLL graphic shows data center year-to-date absorption in megawatts.

Jon Meisel, East Region lead for JLL’s Data Center Solutions, predicted:

The boost in demand by companies large and small for outsourced data centers, more specifically the increase in migration to the ‘cloud’ and the need for proximity to customers with multi-state or multinational operations, are driving a huge wave of consolidation among data center providers that will carry through 2016. Third-party providers are buying up whole competitors and individual data center facilities alike, in key locations that will support their strategic growth plans and enhance connectivity.

JLL’s latest Data Center Perspective report looks at the 15 key North American markets for data center facilities and compares the highlights seen in 2015 with industry expectations for 2016.

While Northern Virginia is expected to remain a location of choice for data centers in the coming year, JLL’s report reveals that areas like Texas, Canada and the Pacific Northwest are gaining a greater share of data center operations.

JLL’s analysis examines the top trends influencing U.S. data center locations in 2016:

- Telecommunications companies unload data center assets: In a major industry shift, large telecommunications providers such as Verizon, CenturyLink, AT&T, Windstream, and others began to shed data center space in 2015 to re-focus on their core competencies rather than trying to compete with the major third-party data center service providers. For those providers, the shift presents opportunities to gain not only market share, but prime assets in tight real estate markets.

- Smaller, tertiary markets are ripe for data center expansion: Data center providers are looking to subordinate markets for expansion opportunities, as they follow online content providers like Netflix and Comcast who are searching for new customers in new markets. Furthering this push into smaller markets are federal requirements for disaster recovery facilities to be located far from company headquarters. With these two factors, it is likely that larger data center providers will start to acquire local data centers in these tertiary markets.

- Cost will continue to drive data center locations: As reported in JLL’s earlier 2015 data center outlook, real estate and operational factors such as construction costs, electricity rates and tax incentives are continuing and will continue to influence data center location decisions.

- Outsourcing and offshoring to become major location drivers: Companies continue to outsource cumbersome and expensive IT activities to industry experts. Latin America will become a particularly active region, with projected data center industry growth of 19.7 percent from 2015 to 2018. As costs rise and space becomes limited, multi-tenant data center providers are seeking space in emerging markets. U.S.-based providers are widely adaptable to international expansion and will continue to invest in foreign markets, like the United Kingdom and Asia-Pacific.

- Markets to watch: Northern Virginia will continue to absorb space as content and cloud providers process more data. Last year, for example, demand exceeded 60MWs mostly from enterprise users. Driven by cheap “green” power, Canada will see disproportionate data center growth as technology companies seek a foothold in Eastern Canada.

Back in the United States, JLL’s report says Northwest U.S. markets such as Oregon and Washington will experience increased demand from California-based technology companies and Asian companies accessing new trans-Pacific wiring. For financial services companies and others willing to pay a premium for maximally low transmission latency, markets like Northern New Jersey, Northern Virginia, Toronto, and Greater Chicago will maintain their status as elite legacy data center locations.

Bo Bond, Central Region lead for JLL’s Data Center Solutions, concluded:

Multi-tenant data center providers and enterprise users alike must think strategically about where to invest in real estate as they balance factors affecting how they provide services. Tax, operating, and power costs continue to be driving factors for both groups and, for data center providers, proximity to customers and how to service demand are critical considerations as well.