by Shane Henson — October 4, 2013—Office vacancy rates continued to decline in most major U.S. markets during the third quarter (Q3) of 2013, based on preliminary data from CBRE Group Inc., a commercial real estate services and investment firm operating worldwide. Eight of the 13 largest markets showed lower office vacancy, led by Dallas, Texas, which experienced a 100 basis points (bps) decline to 18.1%. The U.S. industrial market also continued to show improvement in Q3 2013, according to CBRE, with demand coming from third-party logistics companies, the food service sector, home construction, and automotive suppliers.

“Despite rising interest rates and continued weak growth overseas, the U.S. office market continued to benefit from slow but steady job growth and limited new office development, which has allowed moderate leasing demand to cut the supply of excess space,” explained Brook Scott, CBRE’s interim head of research, Americas. “Meanwhile the U.S. industrial market benefited from consumer and business spending, a recovering housing market, and increased demand for logistics space tied to the growth of e-commerce during Q3 2013.”

Office vacancy

Per CBRE’s findings, the Dallas office market’s strong performance was driven by demand from the professional services sector including insurance, information technology, and financial services firms. Professional services and healthcare also drove a 40 bps decline in both Phoenix, Arizona, and Washington, DC, which reported 23.5% and 14.0% vacancy rates, respectively. Boston had the largest increase in vacancy, at 50 bps, due to a few large blocks of space becoming vacant.

While U.S. employment growth was below expectations in August and revised downward in June and July, the professional and business services sector added 614,000 jobs over the past 12 months. Eight major office markets reported no new office space deliveries during the third quarter, and the vast majority of markets reported an upward trend in rents. Ten projects in Houston delivered 1.6 million square feet of office space during Q3 2013, the greatest amount of all major markets, 75% of which was pre-leased.

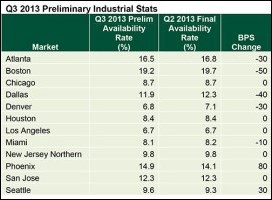

Industrial availability

Meanwhile, says CBRE, industrial availability continued to decline in many major U.S. industrial markets as well, with quarter-over-quarter basis availability rates decreasing in five of the 12 markets, while five markets remained unchanged from the previous quarter. The largest availability rate decline was in Boston, with a 50 bps drop to 19.2%, followed by Dallas, down by 40 bps to 11.9%. Demand for space in Boston was driven by the food sector and warehouse and distribution needs in the 50,000- to 100,000-square-foot range. Demand in Dallas was mainly from third-party logistic companies and e-commerce related companies.

A common theme for most markets was a shortage of Class A space to meet burgeoning demand. Industrial rents have increased moderately in most markets, and design build activity remained strong, with speculative construction gaining momentum. Chicago currently has 5.2 million square feet under construction, including 2.2 million square feet of speculative projects, while Dallas and Houston currently have 10.1 and 7.8 million square feet of new construction underway, respectively, reports CBRE.