by John Forrest — Companies operating across Asia Pacific are presenting their corporate real estate (CRE) managers with twin challenges: Drive down the total real estate occupancy expense while making the CRE portfolio highly responsive to the rapidly changing business environment. However, these seemingly opposing goals cannot be met through the traditional approach of managing the portfolio with a focus on tactical execution.

To successfully drive down cost and increase portfolio responsiveness, CRE leaders need to focus on strategic relationship management with business units, portfolio strategy, capital planning and management. These are the capabilities that the C-Suite and business unit leaders value the most. To build these capabilities in house, CRE leaders across Asia Pacific are increasingly leveraging vendor-partnering relationships to out-task and outsource service delivery to specialist real estate service providers.

Today, vendor-partnering models are most commonly used by U.S. and Australian companies and are an increasing trend among large European corporations. There is evidence suggesting that as Asian companies grow and expand beyond their traditional domestic markets, they too are adopting vendor-partnering models. Asian companies are most comfortable developing a vendor model in their home market as a precursor to expanding the model internationally. As the outsourcing wave has already moved through the U.S. MNC market, we expect to see European and Asian companies as the next wave of partnering and outsourcing over the next five years. vendor Partnerships in asia Pacific

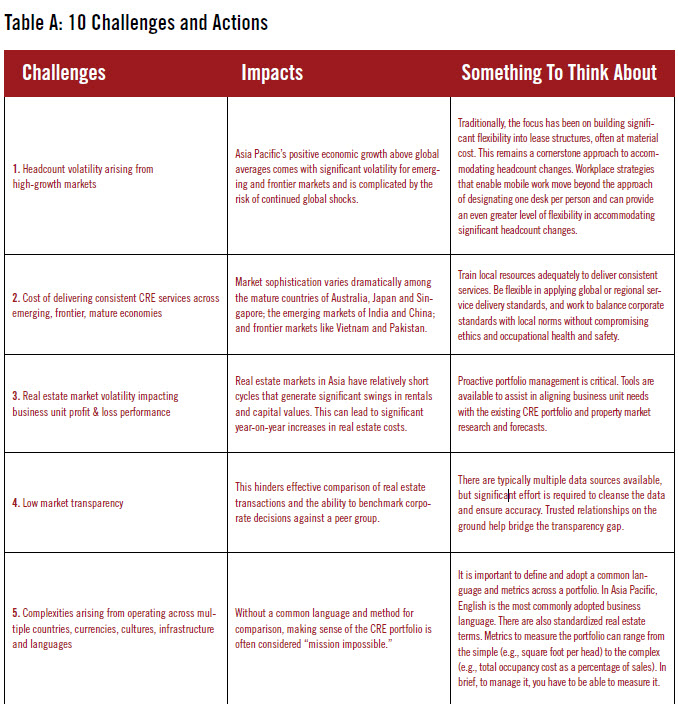

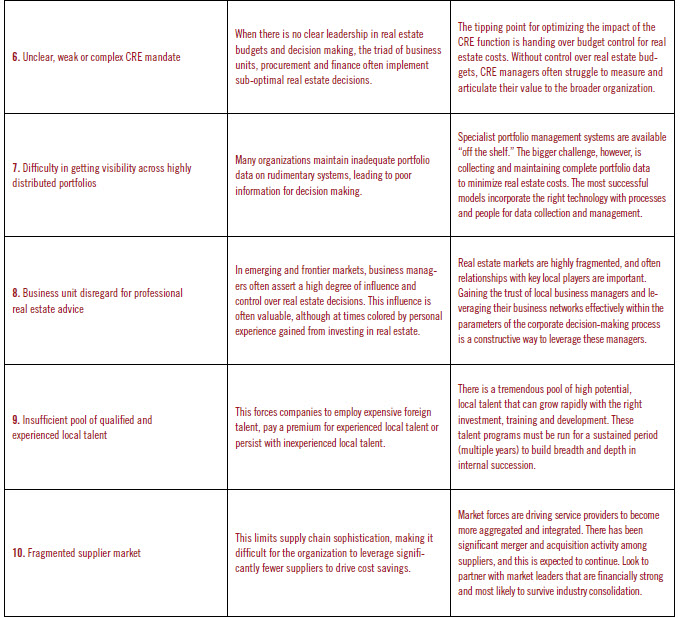

Much has been written about the complexities and dynamism of the Asia Pacific region, and these characteristics create challenges in making partnerships work successfully. Many of the challenges are derived from the geographic scale of the region and the mix of mature, emerging, frontier markets. We have identified ten commonly encountered challenges and suggested actions (See Table A).

What Works in asia Pacific?

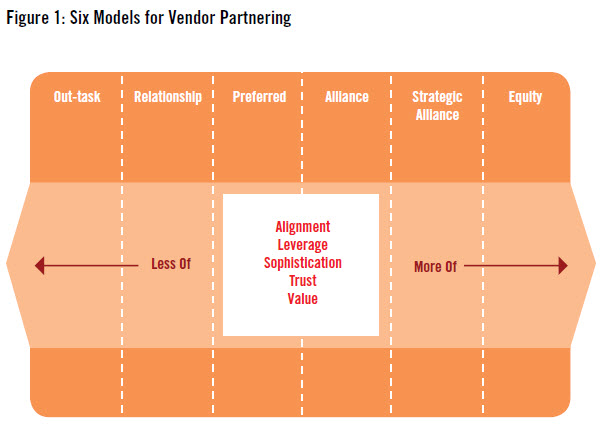

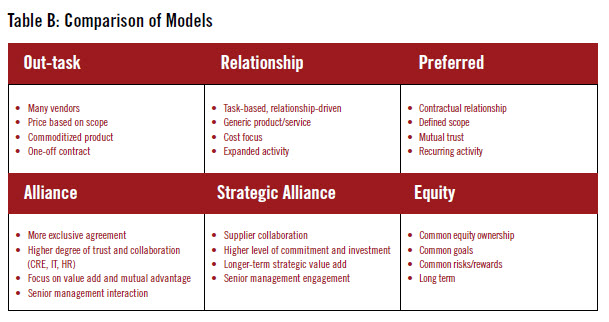

To help address some of the challenges we have outlined, CRE managers are leveraging various types of vendorpartnering models. We see six different models being used in the industry today. These range from the traditional out-tasked model through to specialized vehicles involving common equity ownership. These models are not unique to CRE; generically, they are also evident in other service-based industries. Partnering is a journey-line for many organizations; and depending on their maturity, complexity, culture and geographic footprint, organizations typically migrate left to right across the spectrum. While there are many characteristics upon which the models above can be compared and analyzed, there are five key aspects to note that influence the depth of the partnership:

- Degree of alignment between client organization and vendor

- Degree of leverage gained by client organization

- Level of strategic engagement

- Trust levels

- Value creation

As with all models, each has inherent strengths and weaknesses. The out-tasked and relationship models are commonly favored in first-generation partnerships as they bring industry bestin- class to execute across the varied real estate tasks. As relationships mature, CRE managers typically look for more leverage and move to deeper partnering models such as alliance or strategic alliance, which require less tactical oversight and supervision.

Major cre trends in asia Pacific

- CRE leaders are grappling with the opposing forces of cost reduction and business growth.

- CRE leaders are shifting from a geographic and functional focus to a business-unit focus to better serve their internal customers.

- The shift to smaller and more dynamic in-house real estate teams is directly correlated to the greater reliance on vendorpartner relationships.

- CRE leaders of Asian and Australian companies are gaining increasing influence over their companies international portfolios, driven by real estate spend and growth in Asia.

- Corporate supply chain/procurement is gaining greater influence over real estate.

Geographic coverage has a significant impact on the choice of model. A larger geography drives a significant increase in complexity. In the region, we have seen the models that are most successful at both multi-country and single-country levels. They are significantly easier to manage and are less risky if adopted at a single-country level. Conversely, the benefits of successfully implementing a more strategic partnering model across multiple countries will net significantly greater results if done well.

While the ideal is to keep the planning and strategy components of the function in-house and outsource the tactical work, the growing complexity of organizational growth and challenges brought about by competition in the marketplace has resulted in the need to strike some balance between planning, strategy, and tactics. conclusion

CRE leaders in Asia Pacific are successfully tackling the twin challenges of driving down cost and increasing portfolio responsiveness. The challenge is being met by focusing on strategic relationship management, portfolio strategy and capital planning and leveraging service provider partners for tactical service delivery. This evolution is driving an ever-wider adoption of partnering models across the region. Partnering models are also becoming more sophisticated. This success is being achieved in the world’s most complex and dynamic region. While there are many challenges to overcome, the region is maturing at such a pace that sufficient best practice exists to address the most current challenges. Both CRE teams and service provider partners are evolving rapidly, fueled by the growth momentum in Asia. As partnering models become more widespread and symbiotic, an even greater interdependency between partners is expected in the future.

For more information on this topic, please visit CoreNet Global’s Knowledge Center Online.

Exploring the Asia Pacific Workplace and Building a local Workplace Community

Risks and Rewards: How to Optimize Complex Multi Provider Outsourcing Strategies

Additionally, as European, Asian and Australian companies increasingly adopt partnering models in the region, new models and best practices are likely to emerge.

About the Author

John Forrest is the CEO of Corporate Solutions, Asia Pacific, for Jones Lang LaSalle. He has Pan-Asia Pacific management responsibility for Corporate Solutions, including sales and account management, strategic consulting, corporate research, transaction management, lease administration, project & development services and integrated facilities management.