by By Steve Thomas and Clay Nesler —

In 2007, Johnson Controls sponsored ground-breaking research to get a broad view of how businesses and other organizations were responding to rising energy prices—were they changing their operations, placing more importance on energy efficiency, embracing energy management strategies?

The results provided a benchmark against which to gauge this important sector of economic activity. In 2008, energy-related issues have, if anything, moved more to the center stage. So it’s not surprising that this year’s survey of 1,150 energy management decision-makers found that nearly three-quarters of businesses and other organizations are paying more attention to energy efficiency this year versus the prior year, compared with 62 percent in 2007. The percentage of executives saying energy management was extremely or very important to their organizations also rose significantly, to 57 percent compared with 51 percent in 2007.

Respondents for the second annual Johnson Controls Energy Efficiency Indicator (EEI) online survey were pre-qualified executives and facility professionals responsible for energy efficiency investment decisions in a wide range of facility types, sizes and locations. Executives included an executive panel as well as 338 members of the International Facility Management Association.

Expectations and plans

|

While interest in energy efficiency and energy management has increased significantly from last year, plans to invest in energy efficiency-related measures remained constant. About 60 percent of respondents said they planned to make energy efficiency investments from capital budgets and 60 percent from operating budgets in both years.

One reason might be that the true impact of rising energy costs has yet to be felt by the industry. In last year’s survey, 79 percent said they expected energy costs to rise, and the average anticipated increase was 13.25 percent. According to the Energy Information Administration, while crude oil prices jumped about 30 percent between the first and fourth quarter of 2007, commercial natural gas and electricity prices were relatively flat. In this year’s survey, 80 percent of respondents said they believed that natural gas and electricity prices will increase over the next year. On average, the expectation is for prices to rise 13.79 percent.

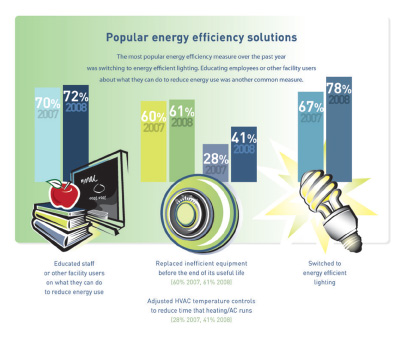

The most popular energy efficiency measure over the past year was switching to energy efficient lighting (78 percent—up 11 percent). Educating employees or other facility users about what they can do to reduce energy use was another common measure—about 72 percent of executives said their organizations do this, slightly higher than last year. Sixty-one percent said they had adjusted heating, ventilation and air conditioning controls to reduce the time these systems operated.

However, while there is still a focus on grabbing the ‘low-hanging fruit,’ 2008’s EEI research indicates that companies are ready to reach for more significant energy efficiency improvements. This year 41 percent of respondents said they were replacing inefficient equipment before the end of its useful life—up 13 percent from 2007. In addition, 88 percent said that energy efficiency was a design priority in construction and retrofit projects—up 11 percent from a year ago.

Environment gains ground as motivator

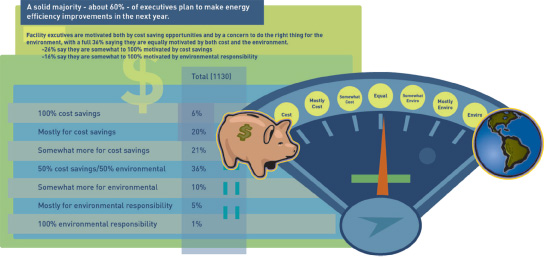

While cost has been the historic driver of energy efficiency investments, environmental responsibility is gaining ground as a motivator. Fifty-two percent of those surveyed said that environmental responsibility was an equal or greater motivator than cost reduction for investing in energy efficiency—up 4 percent from 2007. Sixteen percent cited environmental responsibility as the stronger motivator—up from 13 percent in 2007. Thirty-six percent (about the same as last year) said they were equally motivated by cost savings and environmental concerns.

Green buildings and other emerging trends

The survey asked a number of original questions this year to gain insights into some new financial and environmental issues that may be influencing energy efficiency investments. Much has been written recently about green buildings for both new and existing buildings. Asked whether they had any green buildings in their portfolio, 40 percent of the executives said they had buildings with green elements but no certification. Only 8 percent said they had at least one green building certified to a recognized standard.

Incorporating green elements in new and existing buildings, whether certified or not, was a priority for more than three-quarters of the participants. Green certification was considerably more important for new construction than retrofits. Of those executives who said they had current or planned new construction projects, one-third said they had a goal of green certification compared with one-fifth for retrofits. Nearly one-third of all executives questioned said that they believed that green buildings would be extremely or very important in attracting and retaining future employees.

When asked specifically about renewable energy, the executives surveyed expressed a remarkable openness. Thirty-eight percent said that solar electric was being either included or considered in their new construction or retrofit projects, and 24 percent said they were including or considering solar thermal for their projects. One possible driver is that a significant percentage of executives (38 percent) said their companies felt it was extremely or very important to minimize dependence on traditional energy sources such as gas, oil and electricity.

Other new questions found that:

|

Twenty-eight percent of respondents felt climate change was an extremely or very significant influence on their organizations’ energy efficiency decisions and 31 percent said it was somewhat significant.

Thirty-eight percent said they believed utility or government incentives were extremely or very influential on those same decisions. The only significant regional difference in the results is that an even higher percentage of executives in the West (47 percent) said incentives were extremely or very influential. Nearly 40 percent believed it was extremely or very likely that legislation will mandate energy efficiency and/or carbon reduction within the next two years.

Interesting variations

While responses were fairly consistent across the range of organizations represented, there were a few noteworthy differences. As mentioned, there was only one significant regional difference, but when results were broken out by facility size responsibilities (less than 100,000 square feet, 100,000 to 499,999 square feet and 500,000+ square feet) on many questions, executives responsible for the largest square footage placed more importance on energy efficiency investments. For instance, 73 percent of those executives responsible for the largest square footage said energy management was very or extremely important in contrast to 57 percent for the group as a whole.

Eighty-four percent of executives responsible for 500,000+ square feet of facilities said they planned to make energy efficiency improvements with capital expenditures compared with 56 percent of the group as a whole. When talking about investments made with operating budgets, the difference was similar—85 percent of those with the largest facilities versus 61 percent of the group as a whole. Executives responsible for the largest facilities (500,000+ square feet) were also willing to tolerate a longer payback period for their investments in energy efficiency. A significantly higher percentage of executives with larger facilities were also willing to accept longer energy efficiency investment paybacks (29 percent versus 21 percent for all respondents).

Executives responsible for larger square footage were also more likely to say

climate change was an extremely or very significant influence on their energy efficiency investments; that utility/government incentives were extremely or very influential; and that there would be legislation mandating energy efficiency or carbon reduction in the next two years.

What about IFMA members?

Like the entire group of respondents, the vast majority (80 percent) of IFMA members believed energy prices would rise over the next year, but felt the increase would be less—10 percent in contrast to 15 percent by the executive panel.

The percentage of IFMA members who said energy management was extremely or very important to their companies jumped 6 percent in 2008, to 65 percent—considerably higher than the 53 percent of the executive panel on its own. Not surprisingly then, IFMA members were considerably more likely to have adopted energy efficiency measures in a number of key areas:

Staff-related — Their companies were much more likely to have sent staff to energy management seminars and to have hired an energy consultant.

Equipment and systems — They were more likely to have adjusted temperature controls, installed or upgraded a building management system and installed variable-speed drives.

Lighting — They were more likely to have installed lighting sensors or timers.

Energy supply — They were more likely to have negotiated energy contracts with suppliers.

|

In 2008, IFMA members were more likely to make energy efficiency improvements with capital expenditures (75 percent versus 66 percent) and with operating expenditures (76 percent versus 70 percent) than they were last year; and considerably more likely to do so than the executive panel (48 percent with capital budgets and 55 percent with operating budgets). IFMA members are also more likely to have at least one green certified building than the executive panel (12 percent versus 6 percent) and significantly more likely to have buildings with green elements (59 percent versus 32 percent).

IFMA members who responded to the survey tended to represent larger organizations with bigger facilities, larger revenues and more employees. Thus some of the observed differences between their responses and those of the executive panel may reflect company size. However, for several questions, the trend of their responses diverged from those of executives with larger facilities described earlier:

IFMA members were slightly less likely to feel that climate change was a significant influence on their companies’ energy efficiency decisions (21 percent in contrast to 30 percent for the executive panel).

They were also much less likely to believe that it was important for their companies to minimize dependence on traditional energy (23 percent said it was extremely or very important in contrast to 44 percent for the executive panel).

IFMA members were not considering or implementing renewable energies in new construction or retrofit projects to the extent that other decision-makers have—24 percent said they were considering solar electric versus 52 percent of the executive panel; 15 percent said they were considering solar thermal versus 32 percent of the executive panel; 11 percent said they were considering wind versus 26 percent of the executive panel.

EEI goals

All told, the Johnson Controls Energy Efficiency Indicator research highlights implications and key insights into the current state of energy efficiency in the facility management industry. It’s a snapshot of a rapidly changing economic and environmental landscape. It will be interesting to see how the landscape has shifted in next year’s survey.

About the authors

Steve Thomas is manager of global energy and sustainability communications for Johnson Controls. He has been responsible for product, service and solutions communication efforts at the company for more than 20 years. Thomas is a member of the Nature Conservancy, belongs to the Friends of the Boundary Waters Wilderness, The Theodore Roosevelt Association and the American Institute of Architects. In his role as vice president of global energy and sustainability for Johnson Controls, Clay Nesler leads a worldwide team responsible for coordinating marketing, legislative affairs, resource management, product/service innovation and energy program management.

Nesler’s responsibilities include leading a professional services organization that develops collaborative planning tools and provides consulting services to Johnson Controls customers and third-party clients on a global basis. Since joining Johnson Controls in 1983, he has held a variety of leadership positions in technology, new product development and marketing in both the United States and Europe. Nesler is also listed as a co-inventor on 10 patents.